SEC Insists On Professional Skepticism In Audits To Gain Stakeholders’ Trust!

- Posted by kalyani

- On March 28, 2024

- 0 Comments

It is a truism that audit as a profession needs the maximum amount of skepticism. An auditor must have a mental attitude of neither believing nor denying the possibility of misstatement. An auditor needs a questioning mindset to conduct a critical assessment of the audit evidence. Audit evidence is the information collected that leads an auditor to believe the existence of facts and figures reported in the financial statements. Audit evidence is the trail an auditor marks to justify the opinion provided in the audit report.

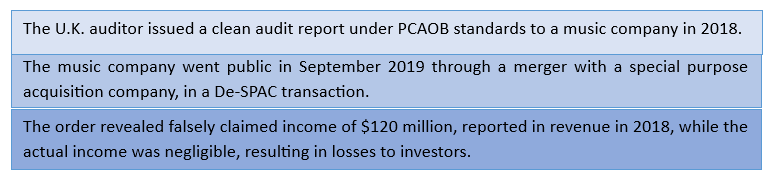

The U.S. Securities and Exchange Commission (SEC), which protects more than sixty-six million American households who place trust in the securities market for their future, issued an order to a well-known U.K. based audit firm, its CEO, and senior auditor for failures in connection with a De-SPAC transaction. A SPAC is a special purpose acquisition company setup with a purpose to acquire an operating business. Here is what happened:

The SEC order finds that besides providing false claims in the audit report that the music company fairly presented its financial statements in all material aspects in 2018, the audit firm also defaulted on other grounds:

- The audit firm claimed to have conducted the audit as per the PCAOB standards when, in fact, the audit team had no training or experience in it.

- The audit team should have exercised more professional skepticism when the music company presented fabricated agreements and inauthentic confirmation letters.

- The engagement partner (CEO), should have supervised the engagement appropriately, maintained adequate documentation, and exercised due professional care.

- The order also found that the engagement quality reviewer needed to conduct a more thorough engagement quality review and have more experience.

The firm, its CEO, and the quality reviewer agreed to settle and pay penalties of $750,000, $25000, and $10000, respectively. The firm withdrew its PCAOB registration, and the CEO and the reviewer agreed to be suspended from appearing or practicing as accountants before the SEC, with the right to apply for reinstatement after five and two years, respectively.

PCAOB Auditing Standard AS 1015 – Due Professional Care in the Performance of Work prescribes that due professional care must be exercised in the audit’s planning and performance and the audit report’s preparation. It clearly explains professional care, professional skepticism, and reasonable assurance. According to the standard, professional care requires professional skepticism, and the auditor must not assume that the management is dishonest nor assume unquestioned honesty.

KNAV’s Perspective

Professional skepticism drives the quality of audits and is imperative to avoiding financial fraud. Hence, the following approach is suggested:

- Assess the knowledge, skill, and ability of team members to evaluate audit evidence they are examining,

- Set a process in place to discuss questionable evidence,

- Delve deeper into such evidence to establish or eliminate the doubt,

- Alert the team to be more vigilant if the suspicion is confirmed,

- Document findings and evidence,

- The engagement partner must be technically sound and know, at the minimum, the prescribed accounting and auditing standards,

- The engagement partner is responsible for resource allocation, monitoring, and supervision of the team members and cannot plead ignorance in case of violations.

Professional skepticism is a mental attitude of doing the work diligently and with integrity. The right quantity and quality of audit evidence is what an auditor needs to establish, to provide an opinion, and it is a matter of professional judgment. Reliance on evidence that is persuasive rather than just seemingly convincing is what makes an auditors’ opinion valuable.

0 Comments