PCAOB Replaces Auditing Standard, Modernizes Requirements for Auditor’s Use of Confirmation

- Posted by kalyani

- On April 15, 2024

- 0 Comments

An audit involves collecting, testing, and establishing audit evidence about financial statement assertions. To provide assurance to the stakeholders, auditors need to rely on third-party confirmations, for certain financial items like bank balance, cash, etc. The Public Company Accounting Oversight Board (PCAOB) has replaced its auditing standard AS 2310, The Confirmation Process, with a new standard AS 2310, The Auditor’s Use of Confirmation, to strengthen and modernize the requirement for the confirmation process.

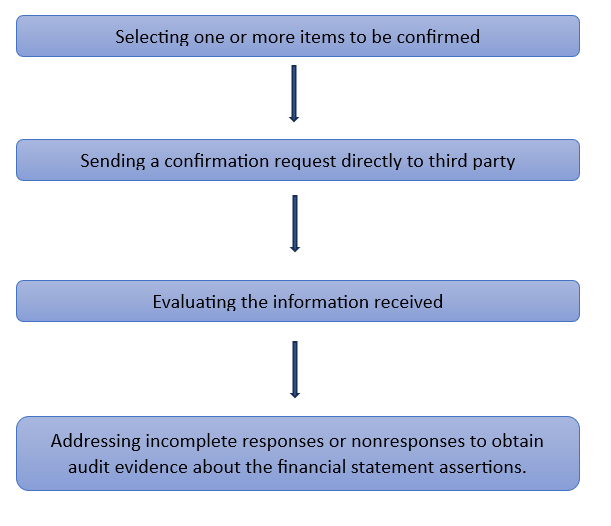

As described in the new standard, the confirmation process involves the following:

Rationale for change

The audit confirmation process establishes existence of certain items in the financial statements and this procedure is inevitable in almost all audits. The current standard was devised when a confirmation was sought through fax or physical mail thus resulting in limited adaptability of technological advancements. To include electronic communications and third-party intermediaries in the confirmation process while strengthening the entire process, the PCAOB introduced the new standard after multiple rounds of public comment.

Key Provisions of the New Standard

The new standard’s purpose is to enhance the PCAOB’s requirement on the use of confirmation by elaborating principles-based requirements applicable to all confirmation methods, including paper-based and electronic means of communication. The new standard also integrates with the PCAOB’s risk assessment standards by encompassing risk-based considerations and stressing on the auditor’s responsibilities for obtaining relevant and reliable audit evidence through the confirmation process. Among other things, the new standard includes:

- a new requirement for confirming cash and cash equivalents held by third parties (“cash”) or otherwise obtaining relevant and reliable information by assessing directly, information maintained by a knowledgeable external source,

- carry forward the existing requirement of confirming accounting receivables while addressing situations where it is not feasible, or obtain relevant and reliable information by assessing directly, information maintained by a knowledgeable external source,

- examples of situations where the auditor may use other substantive audit procedures to supplement negative confirmation requests, as the standard states that using only negative confirmation requests does not provide sufficient appropriate audit evidence.

- fixes responsibility on the auditor for getting control of the confirmation process, selecting the confirmation items, sending requests, and receiving confirmations.

- includes examples of alternative procedures that may provide relevant and reliable audit evidence for a selected item.

The new standard will take effect for audits of financial statements for fiscal years ending on or after June 15, 2025.

AS 2110, Identifying and Assessing Risks of Material Misstatements requires an auditor to set a process to recognize and evaluate the risk of material misstatements. AS 2301, The Auditor’s Responses to the Risks of Material Misstatement, requires the auditor to design and execute appropriate responses that address risks of material misstatements. The standard requires the auditor to set a process to identify, seek confirmation, and action nonresponses for financial items that require external source confirmation.

KNAV Opinion

An auditor must set a process for confirmation, ensuring consistency, reliability, and quality of audit evidence. As a practice, an auditor must –

- Firstly, identify the items that need external confirmation, say cash balances, bank balances, accounts receivable, accounts payable, and assets pledged as collateral, amongst others.

- Next, depending on the nature of the item, an auditor will decide the nature of confirmation required. For example, for confirming cash balance, an auditor must establish existence, whereas, for a revenue transaction, the auditor must establish occurrence.

- Next, the auditor must design the confirmation request – a positive confirmation states the balance and confirms it, a blank confirmation requires the third party to state the balances. A negative confirmation must be used only if the auditor has assessed the risk of material misstatement and obtained sufficient audit evidence, as a negative confirmation will be received only in case of disagreement.

- Further, the auditor must decide to whom these requests must be addressed, and the credibility of the response must be established. In case of doubt, the auditor must seek evidence from substantive procedures.

- The auditor then needs to design an alternative plan in case of unfavorable responses or no responses, to reduce the risk of material misstatements.

A robust confirmation process must be designed and communicated to audit team members, along with action to be taken in case of deviations or escalations to be made. Every facet of an audit review defines the overall quality of the audit, directly influencing investor confidence; hence, detailed process designing, and implementation are inevitable.

0 Comments