Audit Quality Management (QM) Standards: An Insight into the Monitoring and Remediation Procedure

- Posted by admin

- On December 13, 2023

- 0 Comments

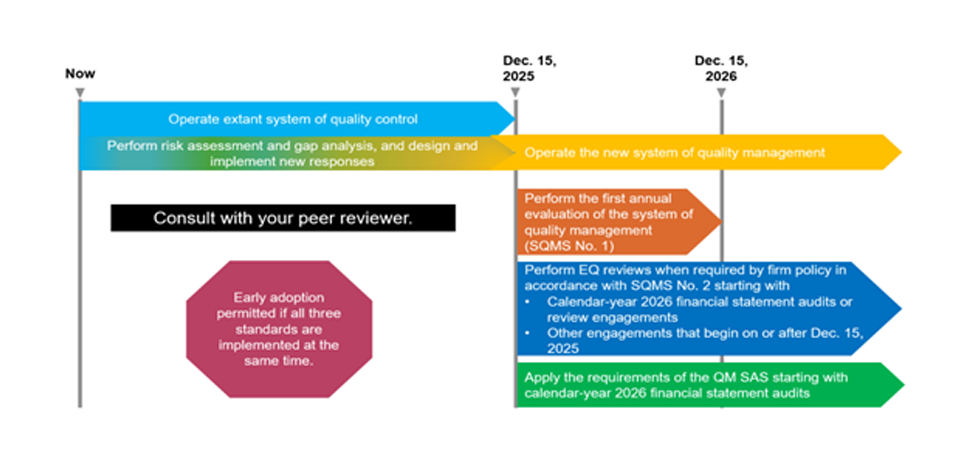

The forthcoming Quality Management (QM) standards herald a notable shift in how Public Accounting (CPA) firms will approach the quality of audits and attestations in the future, pivoting from a policies-based model to a risk-centric approach. Compliance with these transformative standards is mandatory by December 15, 2025.

The QM standards comprise the following components:

Statement on Quality Management Standards (SQMS) No. 1, A Firm’s System of Quality Management:

- SQMS No. 1 supersedes Statement on Quality Control Standards (SQCS) No. 8, A Firm’s System of Quality Control (QC Section 10). It mandates that the CPA firm devise, implement, and operate a tailored system of quality management aligned with the nature and circumstances of its accounting and auditing practice.

- An Engagement Quality (EQ) review, a specified response crafted and executed by the firm to address quality risks, is performed by an EQ reviewer at the engagement level on the firm’s behalf. SQMS No. 1 necessitates the firm to determine the appropriateness of an EQ review as a response to quality risks.

SQMS No. 2, Engagement Quality Reviews:

- SQMS No. 2 focuses on the appointment and eligibility of the EQ reviewer and the execution of EQ reviews.

Statement on Auditing Standards (SAS) No. 146, Quality Management for an Engagement Conducted in Accordance with Generally Accepted Auditing Standards:

- SAS No. 146 replaces and supersedes AU-C section 220. It concentrates on quality management at the engagement level, emphasizing the quality responsibilities of the engagement team and engagement partner.

Statement on Standards for Accounting and Review Services (SSARS) No. 26, Quality Management for an Engagement Conducted in Accordance with Statements on Standards for Accounting and Review Services:

- SSARS No. 26 amends the SSARSs to align with SQMS Nos. 1 and 2.

Who’s Impacted?

All CPA firms conducting engagements in compliance with the SASs, SSARSs, and SSAEs.

Major Transformations:

- Adoption of a novel risk-based approach, integrating a risk assessment process that directs firms to emphasize quality management tailored to their specific circumstances.

- Revision of components within the system of quality management, introducing two new components, notably information and communication.

- Strengthened leadership and governance prerequisites.

- Augmented monitoring and remediation procedures.

- Introduction of fresh obligations for networks and service providers.

The elements comprising the quality management system for monitoring and remediation process:

The procedure that:

- furnishes the firm with pertinent, dependable, and prompt information regarding the structure, execution, and functioning of the SQM (System of Quality Management), and

- deals with taking suitable actions to counter deficiencies to ensure their timely remediation.

Significant distinctions and improvements

In-depth analysis contrasting the facets of quality control in QC Section 10 with the constituents of quality management in SQMS No. 1:

| QC sec. 10 — Elements of quality control | NEW SQMS No. 1 — Components of quality management | Notable differences and enhancements |

|---|---|---|

| Monitoring | The monitoring and remediation process | • Enriched and improved guidance across this element

• Increased focus on the firm’s remedial procedures • Fresh mandate for firms to create policies or procedures concerning the objectivity of individuals conducting monitoring activities • Introduction of the term “findings” regarding information about the SQM suggesting a potential deficiency • Novel prerequisites for the firm to assess the seriousness and prevalence of identified deficiencies via root cause analysis and formulate responsive remedial actions |

Implementation Period

Quality management systems in adherence to SQMS No. 1 must be formulated and enacted by December 15, 2025. The assessment of the quality management system mandated by SQMS No. 1 is obligatory within one year following December 15, 2025.

Understanding Monitoring

Monitoring isn’t a new facet of quality management, but what sets it apart from the existing requirements under QC Section 10, A Firm’s System of Quality Control, is the need to assess findings to determine deficiencies, evaluate the severity and pervasiveness of identified deficiencies, and utilize root cause analysis results to create and implement responsive remedial actions.

Documenting the Monitoring and Remediation Process

Firms need to decide how and where they will document their monitoring policies and procedures. SQMS No. 1 added a requirement for firms to establish policies or procedures addressing the qualifications of individuals performing monitoring activities.

According to SQMS No. 1, monitoring activities may include ongoing procedures performed in real-time and periodic activities conducted at intervals. The documentation of monitoring activities is required annually.

Performing Ongoing Monitoring Activities

Once monitoring procedures are designed and documented, firms should initiate monitoring activities in early 2026 to test the quality management system and identify deficiencies.

Assessing the Quality Management System

During the evaluation of their quality management system, firms can opt for a sampling approach, which may involve a random or risk-based method. The testing may encompass inquiries of personnel, observation/walkthroughs, scrutiny of pertinent documentation, and re-execution of procedures. Firms have the flexibility to select completed engagements or those in progress.

Upon completion of testing procedures, firms must identify and elucidate findings, assess them to ascertain any deficiencies, and then appraise the severity and pervasiveness of identified deficiencies, incorporating root cause analysis.

Takeaway

SQMS No. 1 stipulates that the individual(s) with operational responsibility for the monitoring and remediation process should communicate the results of monitoring procedures to those accountable for the system of quality management, contingent on the firm’s structure. This communication encompasses a description of performed monitoring activities, identified deficiencies (including severity and pervasiveness), and planned remedial actions. It is crucial to convey these details to engagement teams and other stakeholders within the quality management system, facilitating appropriate action and accountability. This communication may be continuous or occur periodically.

0 Comments