Audit in the Absence of Independence: Not Acceptable, says PCAOB!

- Posted by kalyani

- On February 15, 2024

- 0 Comments

An audit is an examination or inspection of financial records, internal controls, and processes to provide assurance to stakeholders. It is a combination of technical knowledge, judgment, and independence. Public company accounts hold the trust of many stakeholders who have a financial interest in them. An auditor’s opinion is a commitment to the security of that financial interest to the best of their knowledge. An audit devoid of an independent position of the auditor is unjust and unfair to the users of the audited financial statements.

Auditor independence is an intricate subject that cannot be defined plainly. The PCAOB, the regulatory body overseeing U.S. public company audits, recently sanctioned Birmingham’s largest privately owned certified public accounting firm for violations of auditor independence and quality control standards.

PCAOB Standard AS 1005 – Independence highlights that in all matters relating to an audit assignment, an auditor must maintain independence in mental attitude. It urges the auditor to have the mindset of judicial impartiality to shoulder the responsibility of being fair to all stakeholders. What is really at stake is public confidence in the profession and to maintain the profession’s integrity, each member must imbibe independence as an indispensable quality.

A public company auditor must meet the independence criteria stated in the PCAOB standards and also satisfy the independence criteria in the U.S. Securities and Exchange Commission rules and regulations. Rule 2-01(b) of the Commission’s Regulation S-X provides that an accountant is not independent of the audit client if, at any point in time, he or she is not, or a reasonable investor having all the necessary knowledge, concludes that the accountant is not capable of exercising objective and impartial judgment on all the aspects of the assignment.

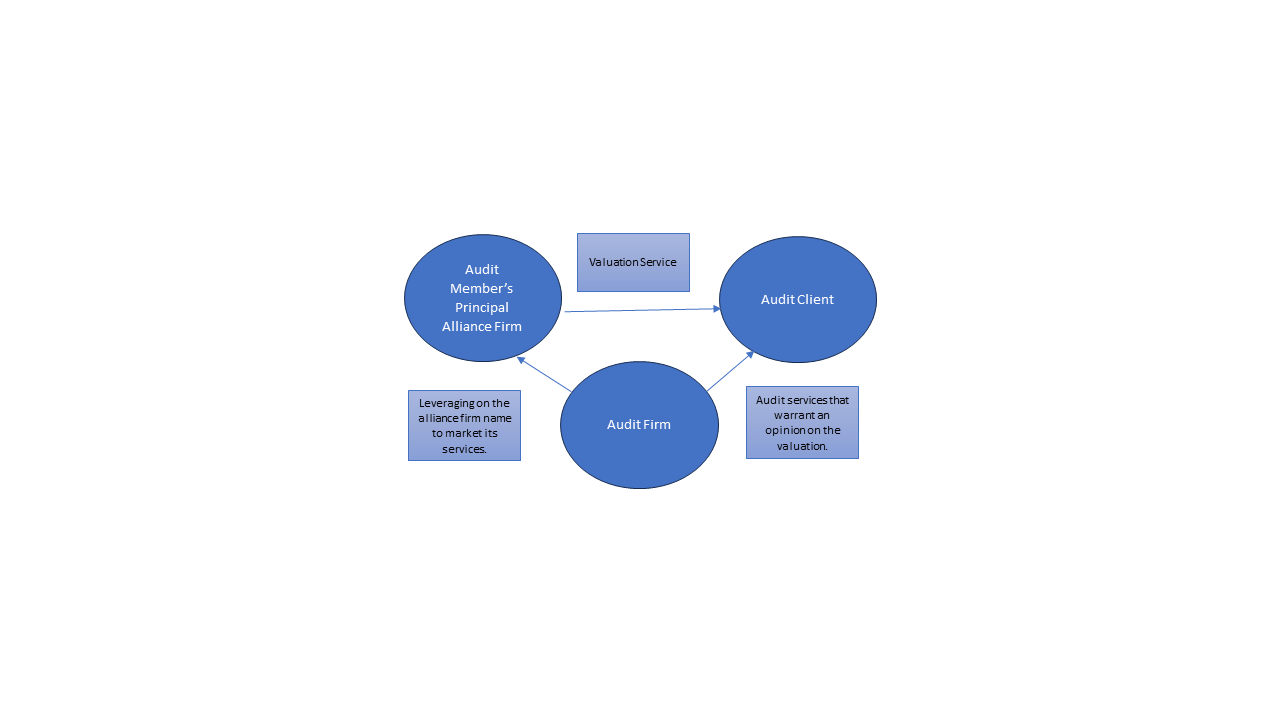

To understand how the Birmingham audit firm violated the independence criteria, let us illustrate:

The matter involved valuation services performed by the Principal Firm that operated an alliance, in which the audit firm was a member. The client and the audit firm are both interested in the accuracy of the financial statements, including the valuations conducted by the principal firm of the alliance, that were significant to the audit. In its position as a member of the alliance operated by the principal firm, the audit firm utilized the brand name and espoused a higher quality service to market its services. Pointing out deficiencies in the valuation report of the principal firm would be detrimental to the reputation of the principal firm and the audit firm. The PCAOB determined that any reasonable investor would conclude that there was a mutual interest between the audit client and the principal firm and the auditor’s independence is compromised. Based on this determination and for lack of quality control procedures the audit firm was sanctioned by the PCAOB. This is a first-ever sanction related to a firm’s membership in an accounting alliance. The PCAOB imposed $200,000 fine and has instructed the audit firm to review and certify its auditor independence policies.

KNAV’s Opinion

Lack of independence stems from the issue of lack of adequate quality control procedures. Adherence and compliance to any law, rules, regulations, or standards require strict internal policies and procedures, a firm-wide awareness of the policies and procedures and commensurate consequences for not following the policies and procedures.

To ensure independence in audits, a firm must:

- Draw up a list of –

- all existing clients,

- all services provided to clients,

- an extensive list of alliances, collaborations, and professional relations with other audit firms.

- Obtain list of other firms providing non-audit services to the clients.

- In the case of an existing relationship with other service providers of the client, a thorough analysis of the relationship and its impact on the audit opinion must be established.

- In case of any conflict, in the firm’s best interest, it would be best to decline the assignment.

- Obtain independent clause agreement from partners and employees involved in client services.

- Continuous monitoring to account for recent changes in circumstances.

Auditor independence is not just a list of bulleted points that must be complied with. Auditor independence is an ethical mindset that provides the auditor the space to give an opinion free of biases and restrictions.

0 Comments