Advance Pricing Agreements: A Powerful Tool for Mitigating Transfer Pricing Risks in the United States

- Posted by kalyani

- On January 24, 2024

- 0 Comments

An Advanced Pricing Agreement (‘APA’) is an administrative approach that attempts to prevent transfer pricing disputes from arising by determining criteria for applying the arm’s length principle to the transactions before those transactions take place (it is a pre-filing resolution tool). They serve as a valuable tool to reach binding agreements on the arm’s length price for present and the future intercompany transactions.

Chapter IV of the OECD Transfer Pricing Guidelines (OECD, 2017[1]) defines an APA as:

An advance pricing arrangement (“APA”) is an arrangement that determines, in advance of controlled transactions, an appropriate set of criteria (e.g., method, comparables, and appropriate adjustments thereto, critical assumptions as to future events) for the determination of the transfer pricing for those transactions over a fixed period of time. An APA is formally initiated by a taxpayer and requires negotiations between the taxpayer, one or more associated enterprises, and one or more tax administrations. APAs are intended to supplement the traditional administrative, judicial, and treaty mechanisms for resolving transfer pricing issues.

While there is no general definition for the subsets of APAs, Section A.2 of Annex II to Chapter IV: Advance Pricing Arrangements in the OECD Transfer Pricing Guidelines (OECD, 2017[2]) outlines three possible forms of APAs in detail:

- Unilateral APAs, which are arrangements between a taxpayer and a single jurisdiction. Unilateral APAs are solely domestic law instruments of jurisdictions and only provide tax certainty in relation to covered transaction(s) in a single jurisdiction.

- Bilateral Advance Pricing Arrangements (‘BAPA’), which are APAs between two jurisdictions and are generally implemented domestically through an agreement between the relevant taxpayer/s and each competent authority. However, some jurisdictions allow taxpayers to be a party to the BAPA. Both methods i.e., APA and BAPA give tax certainty about covered transaction(s) in both jurisdictions.

- Multilateral APAs, which are APAs between more than two jurisdictions. Multilateral APAs offer significant tax certainty for taxpayers and competent authorities compared to traditional bilateral agreements in situations involving more than two jurisdictions. However, given the coordination required and the relative inexperience of most jurisdictions in undertaking such engagements, Multilateral APAs raise significant challenges as well. Some of the challenges are the same as for BAPAs, though they become more pronounced due to the increased number of stakeholders. However, other challenges are unique[2].

An APA is an agreement between the taxpayer and the tax authority on the pricing of future intercompany transactions, and in the case of a roll-back, it would also include past years.

The purpose of an APA is to provide certainty to the taxpayer and tax authority about the pricing of transactions, which can help to avoid disputes over transfer pricing. APAs are intended to be negotiated before the transactions occur and are based on a thorough analysis of the functions performed, assets used, and risks assumed by the related parties. APAs can cover a wide range of transfer pricing issues, including the pricing of tangible and intangible assets, intercompany services and financial transactions.

The USA adopted APA during the earlier stage of transfer pricing enforcement and has the highest resources and case experience among all developed nations. The IRS’s APA program is part of the Office of the Associate Chief Counsel (International) and is overseen on policy matters by the APA Policy Board. The Advance Pricing and Mutual Agreement (APMA) Program is a unit within the Large Business and International Division of the IRS.[3]

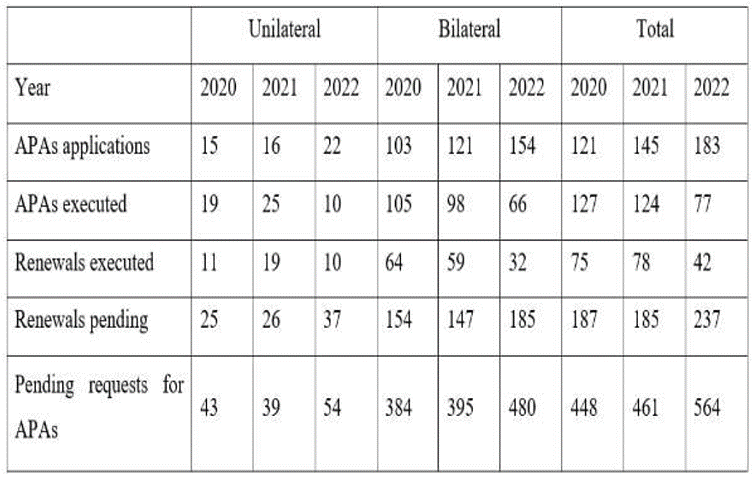

As per the APA report released by the IRS for the year 2022, it has been noted that an increasing number of taxpayers are taking advantage of the program to minimise the transfer pricing controversy with the IRS and foreign countries.

[1] Annex II to Chapter IV of the OECD Transfer Pricing Guidelines, paragraph 39

[2] Annex II of Chapter IV of the OECD Transfer Pricing Guidelines, paragraph 56

[3] Transfer Pricing Analyzer (reganalytics.com)

As observed from the table above, an increasing number of taxpayers are resorting to the program, with an increase in the number from 145 to 183, resulting in a rise of 25%. However, there has been a fall in the percentage of executed APA of about 38%, from 124 in 2021 to 77 in 2022. This decrease is attributable to the decrease in APMA staffing and execution of bilateral APAs, considering those require the participation of multiple tax authorities.

Further, the newly issued guidance by the IRS on the acceptance of advanced pricing agreements sets a clearer viewpoint regarding the APA applications.

The advantages of the entering into APAs can be carved out as below:

- Certainty of transfer pricing procedures and penalty protection: APAs provide certainty to taxpayers regarding their transfer pricing arrangements. By proactively agreeing upon a transfer pricing methodology with tax authorities, taxpayers can avoid potential disputes and uncertainties in the future. This helps in reducing compliance costs and administrative burdens associated with transfer pricing audits and litigation.

- Risk Mitigation: APAs allow taxpayers to mitigate the risk of double taxation arising from inconsistent transfer pricing outcomes across different jurisdictions. With a bilateral or multilateral APA, the tax authorities involved agree on a common transfer pricing methodology, reducing the likelihood of disputes, and ensuring consistency in the treatment of cross-border transactions.

- Resource Efficiency: APAs promote efficiency for both taxpayers and tax authorities. Taxpayers can allocate their resources more effectively by focusing on their core business activities rather than spending significant time and effort on transfer pricing audits and negotiations. Similarly, tax authorities can allocate their resources to more complex and high-risk cases, thereby improving the efficiency of their audit processes.

- Enhanced Tax Compliance: APAs encourage voluntary compliance by taxpayers. By proactively engaging with tax authorities and agreeing on transfer pricing methodologies, taxpayers demonstrate their commitment to following applicable tax rules and regulations. This contributes to build a cooperative relationship between taxpayers and tax authorities, fostering a culture of compliance.

- Promotes Investment and Business Planning: APAs provide a predictable and stable environment for multinational enterprises (MNEs) to plan their international business operations. By knowing in advance how their cross-border transactions will be treated for tax purposes, MNEs can make informed investment decisions, structure their operations efficiently, and avoid unexpected tax liabilities.

- Mutual Agreement Procedure (MAP) Simplification: APAs can simplify the Mutual Agreement Procedure, which is used to resolve transfer pricing disputes between countries under tax treaties. When an APA is in place, the tax authorities involved have already agreed upon the transfer pricing methodology, reducing the need for lengthy MAP negotiations.

In summary, the APA serves as a crucial tool in minimizing tax controversies by assisting taxpayers in pre-determining the tax liability, taking into account the nature of manufactured goods and provided services. Thereby, the taxpayer is aware of the taxable levels and can protect himself from any breaches. APAs also help the administrations of various countries in instances of arbitration. Therefore, it is serving as an important and a growingly popular tool which can help to reduce tax disputes significantly and ensure fairer allocation of income in case of participating nations.

The United States has a well-established APA program that provides a mechanism for taxpayers to reach an agreement with the IRS on transfer pricing before transactions take place. The program is overseen by the APA Policy Board and includes the APMA Program, which has specialized teams covering different industries. The legal basis for the program is Revenue Procedure 2006-9, and the APA process includes several phases.

0 Comments