The Interplay Between Transfer Pricing and ESG

- Posted by kalyani

- On May 16, 2024

- 0 Comments

Introduction

ESG (Environment Social Governance) initiatives and their corresponding solutions are undergoing implementation across organizations at different stages. While some are leading the way, others are still in the initial phases. Regardless of their progress, ESG issues and initiatives are continuously evolving, prompting companies to undergo significant transformations in their operational approaches. By integrating an ESG framework into their fundamental business strategy, organizations can effectively mitigate risks, unlock new opportunities, and generate value for all stakeholders.

On the other hand, Transfer pricing involves determining the prices of transactions within multinational corporations (MNCs), especially those involving cross-border transactions, to ensure fairness and compliance with tax regulations.

The intersection of ESG principles with transfer pricing has become increasingly significant in modern global business. This convergence underscores the recognition that promoting responsible business practices is fundamental to achieving sustainable growth.

The relationship between ESG and transfer pricing is complex, encompassing various aspects such as business restructuring, comparability analysis, allocation of functions and risks, service charges, and cost allocations. It also involves outlining actionable steps for MNCs to harmonize their transfer pricing policies with their overarching global ESG initiatives.

ESG and Transfer Pricing

Transfer pricing involves establishing prices for transactions involving the exchange of goods, services, capital, or intangible assets between entities within the same group. According to transfer pricing rules, organizations must adhere to the “arm’s length principle” when conducting transactions with related parties. This principle dictates that transactions should be priced as if the parties involved were independent of each other, with market forces determining the outcome.

The landscape of transfer pricing legislation has become increasingly intricate over time. MNCs are now subject to heightened scrutiny of their tax practices, and the OECD’s Base Erosion and Profit Shifting (BEPS) agenda has notably influenced transfer pricing policies.

Presently, ESG holds significant importance for companies, with anticipated effects on their business operational frameworks. This can lead to several transfer pricing implications related to value creation, new functions, assets, and risks. Consequently, it is crucial for companies to assess the potential impact of ESG initiatives on their transfer pricing positions as they adopt these initiatives. By implementing robust transfer pricing policies and ensuring accurate data collection and documentation, companies can effectively manage the impact of transfer pricing on their ESG initiatives and mitigate the risk of costly disputes with tax authorities.

Impact of ESG on Transfer Pricing

The integration of ESG factors into transfer pricing analysis has significant implications for MNCs and their approach to pricing intercompany transactions. Here are some key impacts of ESG on transfer pricing analysis:

Value Creation Assessment:

ESG considerations necessitate a reassessment of value creation within MNCs. Traditional transfer pricing analyses focused primarily on financial metrics may overlook the non-financial value generated by ESG initiatives. Therefore, transfer pricing analysis must now incorporate the broader value created by environmental sustainability, social responsibility, and ethical governance practices.

Integration of ESG into FAR Analysis:

The Functions, Assets, and Risks (FAR) analysis, a cornerstone of transfer pricing, traditionally focuses on characterizing entities based on their business activities and assets. However, the addition of ESG considerations requires companies to reassess and document environmental, social, and governmental risks. This reevaluation of FAR is crucial for aligning transfer pricing strategies with ESG principles and ensuring compliance with regulatory standards. Here’s how ESG can be integrated into FAR analysis:

- Environmental Factors: Assessing the environmental impact of a company’s operations, including its carbon footprint, energy consumption, and waste management practices, can provide insights into the risks and opportunities associated with its activities. This analysis helps in identifying potential regulatory compliance issues, resource inefficiencies, and opportunities for sustainable innovation.

- Social Factors: Evaluating the social aspects of a company’s operations involves examining its impact on employees, customers, communities, and other stakeholders. This includes considerations such as employee welfare, diversity and inclusion practices, customer satisfaction, community engagement, and human rights issues. Integrating social factors into FAR analysis helps in understanding reputational risks, brand value, and social license to operate.

- Governance Factors: Governance considerations focus on the internal mechanisms and structures that guide decision-making and accountability within an organization. This includes assessing the effectiveness of board oversight, management transparency, ethical standards, and regulatory compliance. Analyzing governance factors as part of FAR analysis helps in identifying risks related to conflicts of interest, regulatory violations, and corporate governance failures.

Comparable Transactions and Benchmarking:

ESG considerations require adjustments to the selection of comparable transactions and benchmarking methodologies. . The costs involved for ESG initiatives are high which impacts the margins so identifying comparable companies that demonstrate similar levels of commitment to ESG principles remains the key. Further, assessing the ESG performance metrics and incorporating them into the benchmarking process to ensure comparability is required.

Documentation Requirements:

ESG-related transfer pricing adjustments necessitate thorough documentation to support pricing decisions. MNCs must document the impact of ESG factors on their transfer pricing policies, including how environmental, social, and governance considerations influence the determination of arm’s length prices. Transparent documentation is essential to demonstrate compliance with transfer pricing regulations and ESG reporting requirements.

Risk Assessment and Management:

ESG-related risks can impact transfer pricing outcomes and require careful consideration in risk assessment and management processes. MNCs must evaluate the financial and non-financial risks associated with ESG initiatives and develop strategies to mitigate these risks effectively. This may involve implementing robust risk management frameworks that address both traditional transfer pricing risks and emerging ESG-related risks.

ESG Reporting and Certification Requirements:

ESG reporting has become increasingly prevalent among companies seeking to demonstrate their commitment to sustainability and transparency. As part of these reporting obligations, ESG reports often require certification by transfer pricing analysts. This certification process involves evaluating related party transactions to ensure compliance with the arm’s length principle. Transfer pricing professionals must now incorporate ESG factors into their assessments of intercompany transactions and provide commentary on their alignment with ESG objectives.

Reevaluation of DEMPE and CCAs:

The emergence of ESG considerations prompts a reevaluation of key transfer pricing concepts, such as the Development, Enhancement, Maintenance, Protection, and Exploitation (DEMPE) functions and Cost Contribution Arrangements (CCAs). Companies must reassess these arrangements to account for ESG-related responsibilities and costs. For example, investments in sustainable technologies or social initiatives may impact the allocation of costs and profits among group entities, necessitating adjustments to transfer pricing methodologies.

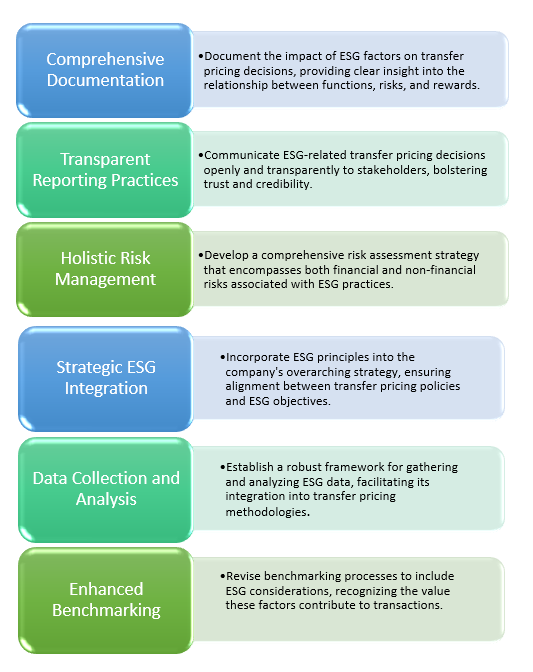

Action Steps for MNCs for Integrating Transfer Pricing with Global ESG Objectives:

MNCs are increasingly recognizing the importance of integrating transfer pricing with global ESG objectives. As sustainability becomes a key focus area for businesses worldwide, MNCs are seeking to align their transfer pricing practices with c principles to promote responsible business conduct and mitigate risks. Here are some key actions that MNCs can take to integrate transfer pricing with their global ESG objectives:

As MNCs endeavor to harmonize their transfer pricing frameworks with global ESG initiatives, they must navigate various complexities inherent in transactions and ESG considerations. By implementing these actionable steps, MNCs can ensure that their transfer pricing strategies not only comply with regulatory requirements but also reflect their commitment to sustainable and ethical business practices, benefiting both their bottom line and the broader societal and environmental well-being.

Conclusion

The correlation between transfer pricing and ESG underscores the interconnectedness of financial and sustainability considerations in today’s business landscape. As companies traverse this intersection, they must proactively integrate ESG factors into their transfer pricing strategies to mitigate risks, enhance transparency, and align with stakeholder expectations. By embracing the synergy between transfer pricing and ESG, businesses can drive sustainable growth while ensuring compliance with regulatory requirements and ethical standards.

0 Comments